Navigating tax systems across the GCC: a guide to Corporate Tax, VAT and Compliance

The Gulf Cooperation Council (GCC) states have always been known for tax-friendly policies, both for businesses and for individuals. But in recent years, GCC governments have implemented a range of tax measures to meet international standards, generate income to support public spending and investment, and to reduce their reliance on oil and gas revenue.

Wherever you are operating your business – Abu Dhabi, Dubai, Saudi Arabia, Bahrain, Qatar, Oman, Kuwait or in one of the many Free Zones – you will need to understand your tax and filing obligations within that jurisdiction, as well as the implications of doing business across the wider GCC.

Value Added Tax (VAT)

In 2016, the GCC States agreed a common legal framework to introduce Value Added Tax (VAT) across the region. Under the agreement, a minimum standard rate of 5% is applied to all goods and services that are not zero-rated or exempt, and VAT registration is mandatory for any business with annual turnover above AED375,000 (c. USD100,000) or its local equivalent.

Saudi Arabia and the United Arab Emirates (UAE) were the first to implement VAT with effect from 1 January 2018; Bahrain and Oman followed suit in January 2019 and April 2021 respectively. Saudi Arabia increased its standard VAT rate to 15% in 2020, and Bahrain increased its standard VAT rate to 10% in 2022.

The introduction of VAT has led to changes in business operations, including accounting and record-keeping requirements. Businesses must now keep proper records of all transactions and ensure compliance with VAT regulations. Non-compliance can result in substantial penalties, which makes it essential for businesses to understand the new tax system and comply with its requirements.

Kuwait and Qatar are the two GCC members that have yet to introduce VAT. The Kuwaiti parliament has repeatedly delayed the VAT implementation date several times due to the strength of opposition. In 2023, the government ruled out implementation during its current four-year plan and is proceeding with the introduction of alternative excise levies. The long-delayed implementation of VAT in Qatar is anticipated in 2025.

OECD Inclusive Framework on Base Erosion and Profit Shifting (BEPS)

All the GCC member states have now signed the OECD Inclusive Framework on Base Erosion and Profit Shifting (BEPS), a 2016 international initiative to address the tax challenges arising from the digitalisation of the economy and to ensure that profits are taxed where economic activities generating the profits are performed and where value is created.

The Inclusive Framework brings together more than 140 countries and jurisdictions to collaborate on the implementation of the BEPS Project. Signatories have committed to implementing 15 actions to tackle tax avoidance, improve coherence of international tax rules and ensure a more transparent tax environment.

The initiative is aimed at ensuring that companies pay taxes where economic activities take place and where value is created. It also sets a global minimum corporate tax rate of 15% for large multinational enterprises.

The impact of the BEPS project has had significant consequences in the GCC. Of the six member states, only Saudi Arabia previously had a qualifying corporate tax (CT) rate and comprehensive transfer pricing (TP) regulations.

Oman and Kuwait also had qualifying CT rates (15% or above) but did not have comprehensive TP systems and, in practice, only foreign companies operating in Kuwait were subject to CT.

Qatar operated a comprehensive TP system, but its CT rate was only 10%, while the UAE and Bahrain previously operated only partial TP systems and neither imposed any CT.

To avoid giving up its taxing rights to other jurisdictions, the UAE announced the introduction of a tax on business profits at a rate of 9% for financial years starting on or after 1 June 2023. Bahrain is to introduce a domestic minimum top-up tax for multinational enterprises from 1 January 2025.

Tax systems of GCC Member States

It is an ever-increasing challenge for businesses operating in the GCC to keep up to date with all relevant tax and regulatory regimes at both a local and regional level as governments in the region bring their tax systems into line with technological advances and international standards.

The GCC has always offered some of the lowest tax rates globally and governments will need to balance their need for revenue with the need to attract investment and promote economic growth.

UAE Tax System

Saudi Arabia Tax System

Qatar Tax System

Oman Tax System

Kuwait Tax System

Bahrain Tax System

Bahrain has a limited corporate tax at 46% that only applies to entities engaged in the exploration, production or refining of hydrocarbons in Bahrain. Bahrain does not impose capital gains tax, withholding taxes or other taxes on the repatriation of profits.

Other applicable taxes may include: VAT (10%), Customs Duty, Stamp Duty, Social Insurance contributions and Municipality taxes.

VAT is administered by the National Bureau for Revenue (NBR) and all businesses with an annual taxable turnover exceeding BHD37,500 are required to register within 30 days of the date the threshold is exceeded or is expected to be exceeded. Non-resident businesses supplying goods or services to non-VAT registered customers in Bahrain must register within 30 days of their first taxable supply.

There is currently no specific legislation regarding transfer pricing or thin capitalisation in Bahrain. However, Bahrain joined the OECD Inclusive Framework on BEPS in 2018 and has therefore committed to implementing TP Documentation and Country-by-Country Reporting (CbCR) as part of the BEPS minimum standards.

Conclusion

The tax frameworks across the GCC member states show both similarities and distinct approaches. As part of ongoing efforts to diversify revenue sources beyond oil, most have introduced – or are considering the introduction of – CIT and VAT, while personal income tax remains absent across the region.

All GCC members states have now joined the OECD Inclusive Framework on BEPS, which is driving widespread change. Additionally, there are unique tax obligations for specific industries, such as oil and gas, across different jurisdictions.

Sovereign’s team provides tailored tax services across the GCC, ensuring that your business remains compliant while optimising its tax strategy. From understanding VAT in the UAE to managing corporate tax obligations in Saudi Arabia and beyond, we’re here to help you navigate these dynamic taxation landscapes with confidence.

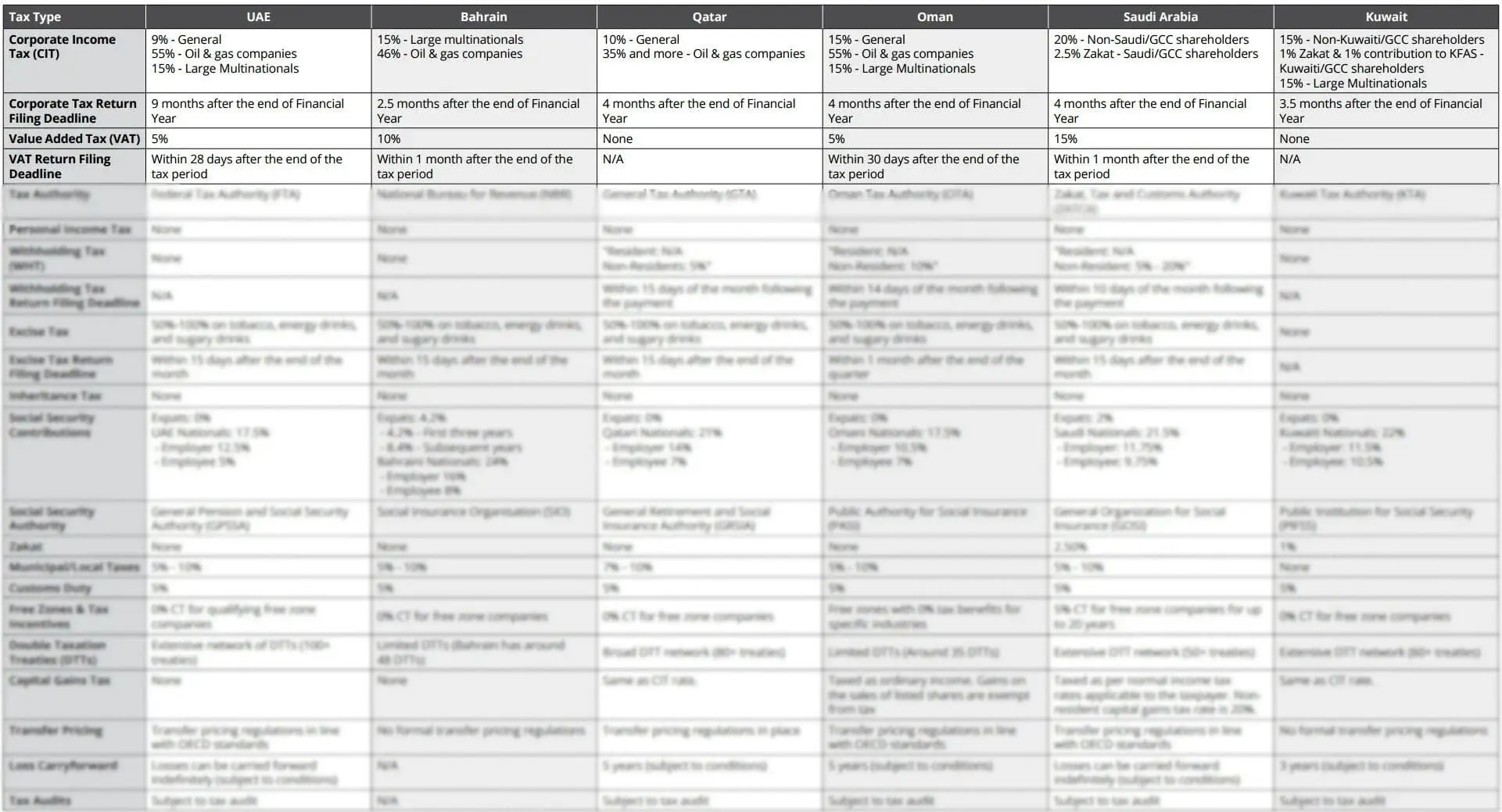

This table provides a comparison of key tax types across the GCC countries, including corporate income tax, VAT, and withholding taxes, which are essential for businesses to understand when operating or planning to expand in the region.

*Last Reviewed on 20 Jan 2025

All information in this chart is up to date as of the ‘Last reviewed’ date on this page. This chart has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this

chart without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this chart, and, to the extent permitted by law, Sovereign does not accept or assume any

liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this chart or for any decision based on it.

Explore Dubai

Please contact us if you have any questions or queries and your local representative will be in touch with you as soon as possible.