The introduction of corporate tax in 2023 at the federal level in the UAE marked a pivotal shift, triggered by the UAE’s diversification strategy and commitment to aligning with global tax standards. It applies a 9% corporate tax rate on taxable profits exceeding AED375,000 (c. USD100,000) for both resident and non-resident businesses.

To ensure compliance with the new regime, a range of administrative penalties were introduced under Cabinet Decision No. 75 of 2023. In this guide, we set out the potential violations and their corresponding penalties, as well as practical strategies to mitigate or avoid them.

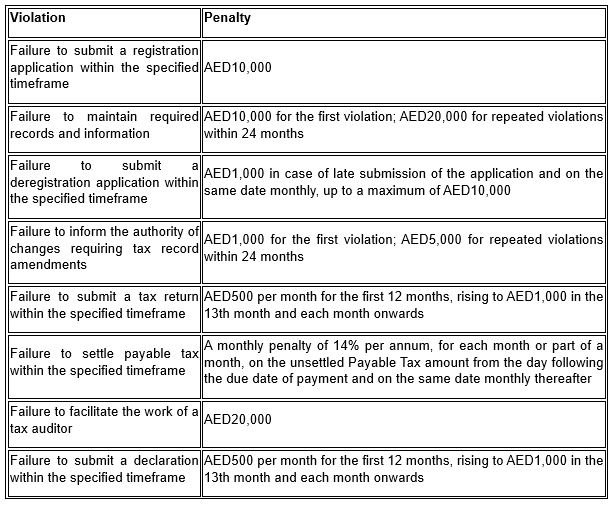

Key penalties for non-compliance

Voluntary Disclosure: a safety net for correcting errors

The UAE’s corporate tax law encourages transparency by allowing businesses to make voluntary disclosures. This provision enables companies to correct errors or omissions in their filings proactively.

While this approach can help businesses avoid harsher penalties, late voluntary disclosures are still subject to penalties, including a 1% monthly fine on the tax discrepancy. Acting promptly to rectify errors is essential to minimise financial and reputational risks.

Penalty Waivers and Instalment Plans

To help businesses manage their tax obligations effectively, the UAE has introduced mechanisms for mitigating penalties under specific conditions outlined in Cabinet Decision No. 105 of 2021:

- Businesses facing penalties due to extenuating circumstances (such as serious illness or death of taxpayer or key employee, restrictions or system failures) may apply for a waiver.

- Businesses can request instalment plans, subject to the following conditions:

- The instalment request must be in respect of unsettled penalties only.

- The total amount of penalties subject to instalment should not be less than AED50,000.

- Penalties subject to instalment should not currently be disputed in front of the Tax Disputes Resolution Committee (TDRC) or Federal Courts.

- The tax due for the tax period subject to the instalment request is settled.

The Federal Tax Authority (FTA) reviews these requests and provides support to eligible businesses.

Proactive measures to avoid penalties

- Stay informed – keep track of updates from the Ministry of Finance and the FTA to ensure awareness of new tax regulations and deadlines.

- Maintain accurate records – use reliable accounting systems to keep financial records compliant with FTA standards. Proper documentation reduces the likelihood of discrepancies and simplifies audits.

- Engage tax professionals – certified accountants or tax advisors can guide businesses through complex tax regulations, identify deductions and prevent errors.

- Leverage tax software – automated solutions can streamline tax compliance, send reminders for deadlines and reduce the risk of filing errors.

Adherence to the corporate tax regulations is essential for businesses operating in the UAE. By understanding the specific penalties for non-compliance and implementing proactive strategies, businesses can minimise risks and focus on growth.

For further information or expert guidance on navigating these regulations, please contact Sovereign PPG.